The Bond Market Is Telling You the Macro Regime Has Changed

Just as we predicted five months ago, the 30-year Treasury yield hit its highest level in 20 years.

Five months ago, we wrote about an emerging change to the macroeconomic regime.

At the time, the overwhelming market consensus was straightforward: the economy was slowing, inflation was fading, and the Federal Reserve would soon be forced to lower interest rates.

We believed this conventional thesis was wrong.

Instead, Atlas argued that the U.S. economy remained significantly stronger than consensus expectations and that inflation would likely prove far stickier than markets anticipated. In our view, real economic growth was simply too resilient to justify the aggressive rate-cut expectations embedded in long-duration bonds.

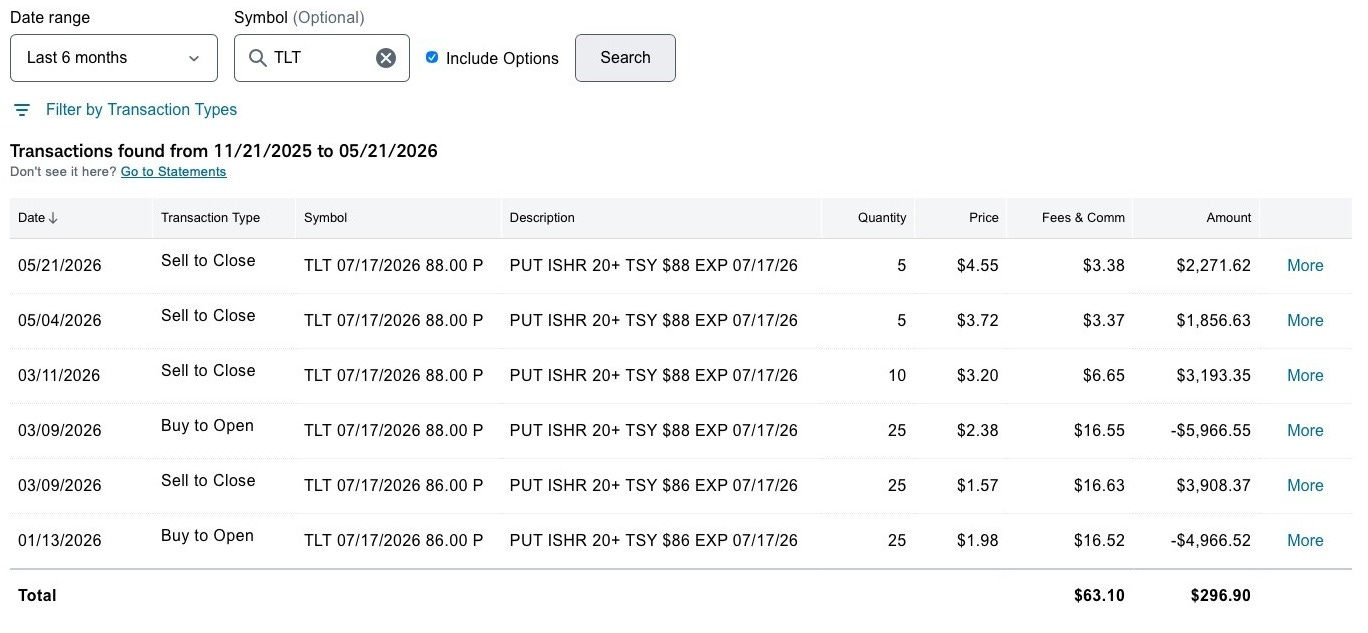

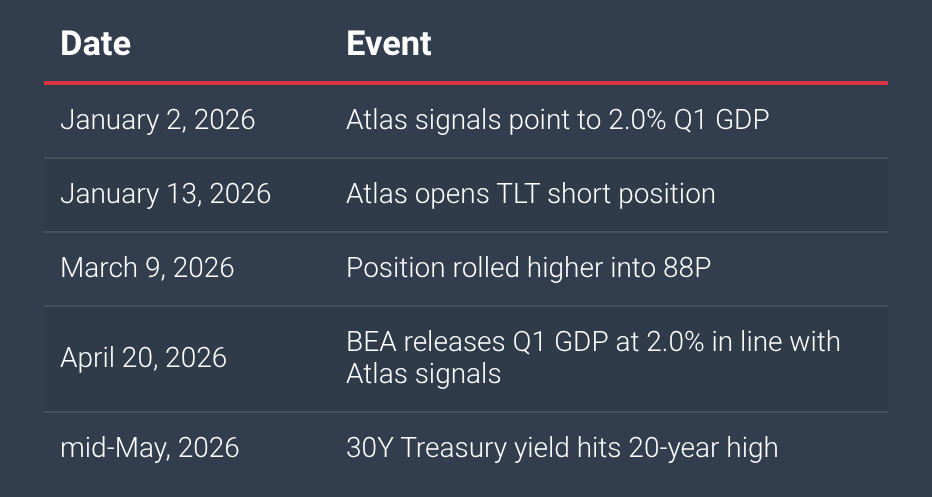

Within the Atlas model portfolio, we established a short position on long-duration U.S. Treasuries through put options on the iShares 20+ Year Treasury Bond ETF (TLT). Specifically, we initially purchased 25 July 2026 $86 puts in January before later rolling the position higher into July 2026 $88 puts as the thesis continued to strengthen.

Since then, long-duration Treasuries have repriced sharply, reinforcing the broader macro signal Atlas identified earlier in the year.

Atlas Analytics TLT Positioning (January – May 2026)

The 30-year Treasury yield has now surged to its highest level in approximately twenty years, while our remaining TLT put position is currently up roughly 100% with nearly two months remaining before expiration. We have already realized gains on a portion of the position while maintaining exposure to what we believe may still be an ongoing structural repricing in the bond market.

Importantly, however, this was never merely a tactical trade.

What we are witnessing may instead represent something much larger: a fundamental shift in the macroeconomic regime itself.

The Market Expected a Slowdown

To understand why this move has been so significant, it is important to recall where consensus expectations stood only a few months ago.

Markets entered the year heavily positioned for economic weakness. Investors broadly expected slowing growth, rapidly declining inflation, and multiple Federal Reserve rate cuts.

This narrative seemed intuitive.

After all, interest rates had risen at one of the fastest paces in modern history. Conventional macroeconomic thinking suggested that such aggressive tightening would inevitably “break” the economy, forcing policymakers to reverse course.

Long-duration bonds rallied aggressively as investors priced in this outcome.

Yet beneath the surface, the underlying economy continued to exhibit remarkable resilience.

Consumption remained firm. Labor markets stayed tight. Fiscal spending continued supporting nominal activity. And many of the real-economy indicators we monitor at Atlas suggested that economic momentum remained substantially stronger than traditional sentiment indicators implied.

The market was pricing a recessionary slowdown.

But the physical economy was signaling something very different.

What Atlas Forecasted

That signal mattered because it had direct implications for rates. If nominal growth was more resilient than consensus believed, then inflation would likely prove harder to extinguish, rate-cut expectations were probably too aggressive, and long-duration bonds were vulnerable to repricing.

Atlas expressed that view through a short position in long-duration U.S. Treasuries via TLT puts. The trade was not the thesis itself. It was one expression of a broader macro framework built on stronger physical-economy signals, sticky nominal growth, and a likely repricing of long-term rates.

Rather than relying exclusively on lagged surveys or sentiment data, our proprietary algorithms use satellite imagery and alternative datasets to track physical economic activity in near real-time. Construction activity, industrial development, land use changes, infrastructure expansion, and trade flows all provide signals about the true underlying pace of the economy.

And critically, those signals remained far stronger than consensus expectations throughout the beginning of 2026.

In fact, as early as January 2nd (when our first satellite collections of the year began orbiting) our internal Atlas models were pointing toward 2.0% real GDP growth for Q1 2026, well above the increasingly pessimistic market narrative that was taking hold at the time.

Over the following months, many of these physical-economy signals remained persistently firm. Consumption activity, infrastructure expansion, industrial development, and broader measures of nominal activity continued suggesting that the economy was not weakening nearly as rapidly as markets believed.

This distinction proved critical.

If nominal growth remains resilient, inflation can become harder to fully extinguish, and long-term rates may need to reprice. That repricing can reflect several forces at once: stronger growth, stickier inflation, fiscal deficits, Treasury supply, and a higher term premium.

Four months later, when the Bureau of Economic Analysis officially released the Q1 GDP figure, the economy printed at exactly 2.0% growth, precisely in line with our forecast generated months earlier from satellite-based economic monitoring.

In our view, markets had become anchored to the macroeconomic assumptions of the 2010s: low inflation, low growth, low interest rates, and abundant global liquidity.

But the post-pandemic economy increasingly appears governed by a very different set of dynamics.

Why Long-Duration Bonds Became Vulnerable

Long-duration bonds are extraordinarily sensitive to changes in interest rates.

When yields rise, bond prices fall. And the longer the duration of the bond, the more severe that price decline becomes.

This is precisely why TLT became such an attractive expression of our thesis.

The ETF holds long-dated U.S. Treasury securities whose valuations are highly sensitive not only to Federal Reserve policy expectations, but also to long-term assumptions about inflation, economic growth, fiscal sustainability, and term premium.

As the market gradually realized that inflation might remain elevated and that economic activity was not slowing as dramatically as anticipated, long-term yields began repricing aggressively upward.

The result was a sharp decline in long-duration bond prices.

Importantly, this repricing may not simply reflect short-term Federal Reserve dynamics.

It may instead represent the bond market beginning to adjust to a structurally different economic environment altogether.

The End of the Post-2008 Regime?

For nearly fifteen years following the Global Financial Crisis, markets operated within an unusually stable macroeconomic regime.

Inflation remained subdued. Globalization exerted persistent disinflationary pressure. Central banks maintained extraordinarily accommodative policies. And interest rates remained historically low across much of the developed world.

That environment may now be changing.

Today’s economy increasingly appears characterized by:

Larger fiscal deficits

Persistent government spending

Deglobalization and supply-chain restructuring

Industrial policy and reshoring

Higher structural inflation volatility

Tight labor markets

Elevated geopolitical fragmentation

Collectively, these forces may produce a world in which nominal growth and inflation remain structurally higher than investors became accustomed to during the 2010s and what Larry Summers termed “secular stagnation.”

If so, long-term interest rates may also need to remain structurally higher.

This would carry profound implications not only for bonds, but for virtually every major asset class.

Importantly, a structurally higher-rate environment does not necessarily imply economic collapse or runaway inflation. It may simply reflect a world characterized by stronger nominal growth, persistent fiscal expansion, and higher equilibrium interest rates than investors became accustomed to during the post-2008 era.

Why This Matters Beyond Bonds

The long end of the Treasury market serves as the foundation for the global financial system.

When 30-year Treasury yields rise meaningfully, the effects ripple throughout the broader economy.

Mortgage rates increase. Corporate borrowing costs rise. Equity valuation multiples compress. Commercial real estate faces additional pressure. Venture capital and private equity become more constrained. Government financing costs expand rapidly.

In many ways, higher long-term yields represent a repricing of the future itself.

And this is precisely why we believe the current bond market move deserves close attention.

The market may no longer be operating under the assumptions that defined the post-2008 era.

Critical Questions Remain:

Will inflation continue proving stickier than expected?

Can the Federal Reserve tolerate structurally higher long-term yields?

Will fiscal deficits continue exerting upward pressure on term premium?

Is the bond market beginning to recognize that the macroeconomic regime itself has fundamentally changed?

These questions will define the next phase of the macro cycle. And as this year has shown, the market narrative can move in one direction while the physical economy points in another.

Investors need faster ways to understand whether the economy is actually weakening, or whether consensus is once again looking in the wrong place.

That is the core of Atlas’ work: using satellite imagery, alternative data, and machine learning to measure real-world economic activity as it is happening, not months later.

If your team is thinking through what a changing macro regime means for portfolios, policy, or capital allocation, we would welcome the conversation.