Is the USD Undervalued Compared to the Euro? Maybe.

Atlas Analytics' Weekly Subscriber Update

Last week, we explored the concept of the Optimal Rate for U.S. interest rates. With forecasts now in place for both GDP and the Federal Funds Rate, we’ve opened the door to a whole new set of macroeconomic insights, starting first with the currency markets.

This week, we tackle a timely question:

Is the U.S. Dollar undervalued relative to the Euro?

Before we dive in, a little context...

How Analysts Calculate the Intrinsic Value of Currencies

Currencies, like any other asset, can become over- or under-valued for a myriad of reasons not driven by the fundamentals: hype, speculation, and what John Maynard Keynes coined “animal spirits”.

Many other analysts have highlighted that currencies can deviate (sometimes wildly) from fundamental value. For instance, the IMF COFER has created an annually updated dashboard on currency valuations, and The Economist magazine publishes a highly-publicized “Big Mac Index” which attempts to, excuse the pun, take a bite out of properly valuing currencies around the globe.

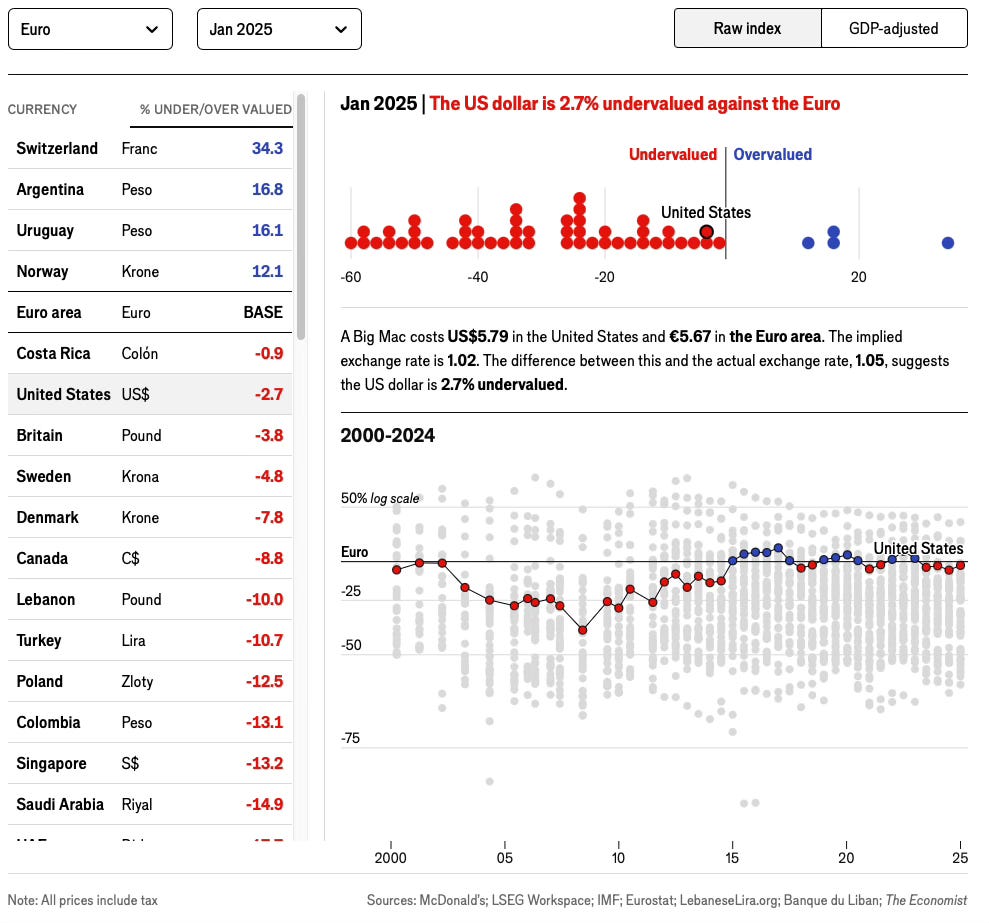

So… Is the Dollar Overvalued?

According to The Economist Big Mac Index, which calculates the implied price difference for a common good across countries (a cheese burger), the answer is yes. The USD is under-valued.

But, that was for the last six months of 2024.

And, based on our analysis at Atlas Analytics, we agree (mostly), or at least we did for 2024.

So what’s happening now?

Surprisingly, the Dollar has quietly depreciated over the last six months against the Euro by approximately -11.3%.

As the headline chart at the top of this article highlights, the Spot Rate is just starting to peak below the intrinsic value (modeled by our regression based on the Optimal Federal Funds Rate from last week, more on that below).

So is the Dollar now fully under-valued vis-a-vis the Euro?

Maybe.

Likely not just yet, but if it keeps on its current trajectory, almost certainly it will be.

How Did Atlas Analytics Calculate the Exchange Rate?

At Atlas Analytics, we’re not only economists but also econometricians. What is an econometrician? In short, we use econometric modeling (mathematical models that take input data to predict expected outcomes) to quantitatively model the economy.

In this case, we take key inputs to model the USD/Euro spot exchange rate.

What’s a spot exchange rate? It’s essentially the market trading price for U.S. Dollars in terms of Euros. And what’s key here is that, like any market price, the trading value can deviate from its fundamental value (see our article “The Tale of Two Prices” for more on intrinsic value versus trading price).

So what are these model inputs?

Economic theory would suggest three key things modulate currency pricing:

Interest Rate Differentials:

First and foremost, international investors seek a high rate of return, so a high interest rate (as largely set by the country’s policy rate, see above) is far and away the most important variable. As the majority of international investment occurs in the debt (Treasuries) market, this high rate of return is set explicitly by the interest rate that their investment commands.

However, it’s not just the rate of return on-the-level that is important; for instance, why invest in the US if the return is the same in your home country (in this case, the Euro Area). Thus, it’s the differential between the two rates that is important.

Economic Growth Differentials:

Enter GDP into the equation. Investors are looking for strong rates of return, and the GDP growth rate is the tide that lifts all ships, including equities and debt valuations.

Again, the differential is paramount for the same reasons as above: why introduce the foreign Country Risk Premium if you can get the same growth domestically?

Money Supply Differentials:

Finally, the money supply (technically M2 or “broad money”) factors into this equation. The money supply is the amount of liquidity allowed by the central bank and factors directly into inflation. The thought process here is that high M2 growth may lead to a devaluation of the purchasing power of the assets invested in. And again, the differential is key.

We ran the regressions based on the theory (accounting for stationarity, heteroskedasticity, etc.) and the results were, well, surprising (even to us). Interestingly, the regression showed that only one variable in our model was statistically significant: the Interest Rate Differential.

This could be for a myriad of reasons, but we suspect that it’s due to lack of data (the Euro Area is only 20 years old after all, so we only have two decades’ worth of data).

How does this relate to last week’s post on the Optimal Interest Rate?

Well, by modeling the Federal Funds Rate using inflation and GDP (essentially the Taylor Rule), Atlas Analytics has developed a proprietary “intrinsic” value for the U.S. interest rate based upon economic fundamentals. This week, building on this, we’ve modeled the USD/Euro Spot Rate using this true Federal Funds Rate. We believe this gives a more accurate picture of the fundamental spot rate for currencies that is actionable for Mr. and Mrs. Investor to trade upon.1

As an aside, we’re happy to share our regression outputs if helpful (but abstaining here in Substack so as to spare the reader).

What Should You, Mr. or Mrs. Investor, Do?

So, should you short the USD compared to the Euro?

Again, maybe.

Looking at the chart above, it appears the optimal spot rate is rising while the actual spot rate is declining. If this deviation continues, then we actually think the USD will become too under-valued.

We’ll keep our eye on it, and, if this happens, we’ll let you know when is the right time to actually go long on the USD.

In the meantime, hang tight, Mr. and Mrs. Investor.

Conclusion: Exorbitant Privilege

The U.S. continues to enjoy what economists call the “exorbitant privilege,” the unique global demand for the Dollar, despite fundamentals that might say otherwise. But history shows even the Dollar is not immune to what we’ve termed as “economic gravity.” If current trends continue, valuation imbalances may create opportunities, or risks, for currency-sensitive investors.

Want More?

At Atlas Analytics, we don’t just track markets. We model them. If you're an investor, policymaker, or data wonk who wants early signals on macro shifts like this one, subscribe to our premium Substack for full access to our real-time forecasts and modeling deep dives.

For enterprise licensing, custom research, or a walkthrough of our USD/EUR model, reach out directly, and we’re happy to chat.

Our Atlas Analytics team would also like to note that we have the predicted forward-looking Optimal Federal Funds Rate, but do not have a forward policy rate for the Euro Area (yet). As such, we left the Euro Area policy rate constant.