Arbitraging the Deviation Between Fundamental Value and Market Sentiment

Equity Markets react to geopolitical and economic news, but not always rationally

Nearly a year ago, in A Tale of Two Prices, I drew a distinction between what an asset is worth and what it trades for.

That gap still exists, and, in recent weeks, it has widened.

Equity markets continue to react violently to geopolitical headlines and macro noise: conflict escalation, temporary ceasefires, oil price swings, policy speculation. Prices move quickly.

Fundamentals do not.

The result is a persistent dislocation between market sentiment and economic reality.

For example, this week, equities rallied approximately +3.5% in a single day on ceasefire headlines, while Atlas Core GDP declined by roughly -0.6% on a weekly basis.

In theory, this shouldn’t happen.

The intrinsic value of an equity is simply the discounted value of its future cash flows. In efficient markets, price should be a close approximation of that value.

In practice, it rarely is.

Not because investors misunderstand the theory, but because they cannot reliably forecast the inputs.

Projecting earnings even one year forward is difficult. Five years forward is guesswork. As a result, price targets diverge wildly across institutions, each built on different assumptions, models, and narratives.

Some will be directionally right.

None will be precisely correct.

Faced with this uncertainty, markets default to something easier: trading sentiment.

Oil spikes? Sell equities.

Ceasefire headlines? Buy risk.

These reactions are fast, intuitive, and almost entirely untethered from the magnitude of their impact on underlying cash flows.

That is the inefficiency.

The solution is to anchor valuation not to narratives, but to the underlying driver of aggregate earnings: GDP.

Calculating Fundamental Value Based on GDP

There is a reason many investors dismiss macro.

At the level of a single company, they are often right to do so.

The dominant risk to any individual equity is idiosyncratic:

balance sheet strength, management execution, competitive dynamics, capital allocation.

Macro matters—but it is often second order.

A weak company can fail in a strong economy.

A strong company can outperform in a weak one.

This is the foundation of bottom-up investing.

But something important happens when you move from a single stock to a basket of equities.

Idiosyncratic risk diversifies away.

The probability that one company’s earnings miss drives the entire S&P 500 lower is extremely small. Across hundreds of companies, firm-specific shocks cancel out.

What remains is the common factor.

Macroeconomic risk.

At the index level, earnings are no longer primarily a story of individual companies. They are a story of the economy itself.

And the most direct measure of that economy is GDP.

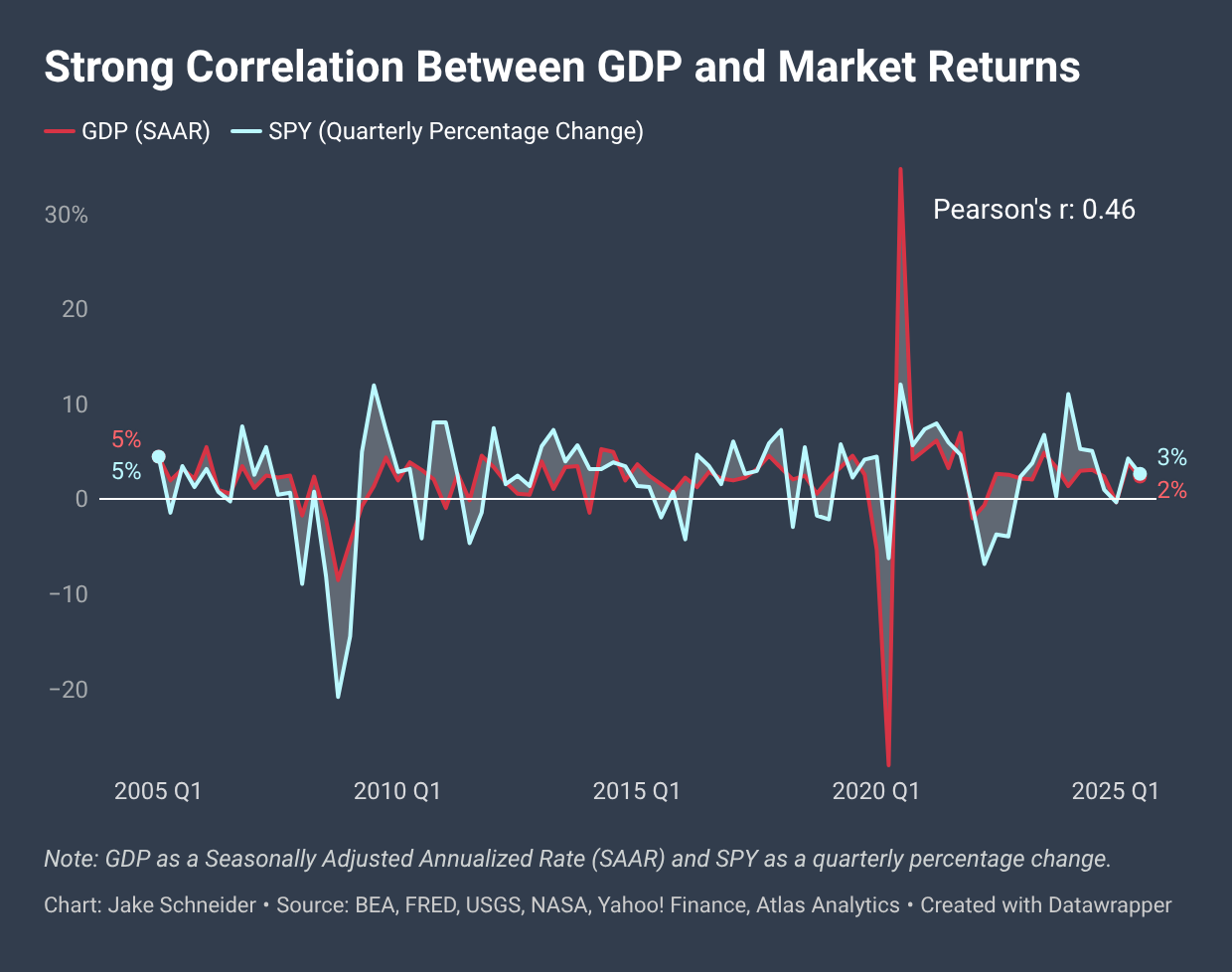

As the chart above shows, the correlation between GDP growth and the SPDR S&P 500 ETF Trust (SPY) is approximately 0.46—a statistically meaningful and economically intuitive relationship.

This is the key insight:

If aggregate earnings are a function of economic activity, and economic activity is captured by GDP, then equity indices should exhibit a systematic relationship to GDP over time.

That relationship can be measured.

Using historical data, we can estimate an econometric model linking GDP growth to index-level price movements. In its simplest form, this is a regression: mapping changes in GDP to changes in equity prices.

The output is not a narrative.

It is a mathematical estimate of fundamental value.

Once that relationship is established, we can input forward-looking GDP estimates—rather than backward-looking sentiment—to generate implied price targets for macro-exposed equities.

And this is where the opportunity emerges.

Markets trade on headlines, positioning, and emotion.

Fundamentals evolve more slowly, and more predictably.

When the market price diverges meaningfully from the GDP-implied fundamental value, that gap can be systematically arbitraged.

That is the foundation of the Atlas approach.

A Common Objection

I hear the same objection frequently from fundamental investors:

“We’re a bottoms-up shop. We don’t use GDP.”

My response is always the same:

What drives the income statement?

Revenue.

What drives revenue?

Demand.

And what is aggregate demand?

GDP.

You may not model it explicitly.

But you are trading it, whether you realize it or not.

Creating Price Targets By Inputting Credible GDP Forecasts

Estimating the historical relationship between GDP and equity prices gives us a framework.

But the real edge comes from what we input into it.

Most market participants rely on lagged and revised macroeconomic data.

GDP is released with a delay.

It is then revised, usually multiple times, over the following months.

By the time the “truth” is known, the market has already moved.

In effect, investors are attempting to price the present using an imperfect view of the past.

At Atlas, we take a different approach.

We generate real-time estimates of economic activity using satellite imagery and machine learning.

Our Core GDP signal is designed to capture the underlying momentum of the economy as it is happening, not as it is later reported.

This distinction is critical.

Because once the relationship between GDP and equity prices is established, even modest improvements in GDP estimation translate directly into more accurate estimates of fundamental value.

Instead of asking:

What did GDP look like?

We ask:

What does GDP look like right now—and where is it going?

By inputting these forward-looking GDP estimates into our model, we generate implied price targets for macro-exposed equity indices.

These estimates are not driven by headlines.

They are not driven by positioning.

They are driven by the underlying trajectory of the economy itself.

And when those estimates diverge meaningfully from market prices, the opportunity becomes clear.

The Result: The Atlas Model Portfolio

This framework allows us to move from theory to execution.

When market prices deviate meaningfully from GDP-implied fundamental values, we take positions to capture the convergence.

When equities trade below fundamental value, we go long.

When they trade above it, we reduce exposure or position short.

The portfolio is not constructed around narratives or forecasts of sentiment.

It is constructed around measurable economic reality.

In an environment increasingly driven by short-term reactions and macro headlines, that discipline matters.

The results have been compelling and increasingly difficult for even the most committed “bottoms-up” investors to ignore.

As the graphic above shows, as of the close of market on Wednesday, the Atlas Model Portfolio is up approximately ~40% year-to-date, compared to a broader market that is down roughly 2% over the same period.

Markets may trade on sentiment in the short run.

But over time, fundamentals assert themselves.

If you’d like access to our forward-looking GDP signals and model-implied price targets, we’re beginning to share a limited set of these insights with partners. Feel free to reach out.